There is alternative signal analysis program which do not resort to follow random processes are fraction of time approach. While doing this process statistical parameters are defined through infinite time average cycle. It does not go with ensemble average of random process. The adoption of fraction of time probability approach is based in the fact of many applications of it.

Like the usage of time series in finance, signal processing and climatology multiple usage of stochastic process are at the disposal of experiment. Cyclostationarity can also be seen during this process. There are many realisation that can be observed after increasing length time travel.

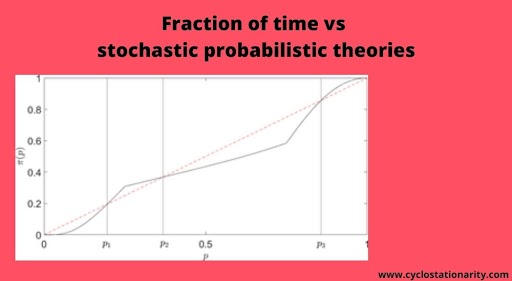

Difference between the fraction of time approach and the stochastic probability approach have huge variety of implications that study the properties of inferential techniques. The fraction of time probability framework is a natural way to define estimators that goes through finite time average of same quantity that involves in infinite time average precisely of Cyclostationarity.

The kind of convergence of estimators are considered as the observation approaches infinity in the convergence of 1 of the sequence of finite time averages. It is pointwise. It is in the temporal mean square sense or the sense of generalised functions. On contrary the stochastic process framework almost everywhere sense or in weak convergence sense.

The fraction of time probability approach was introduced with the reference to time invariant statistics of normal function of time. It was developed and then extended to the case of distributions. In isometric isomorphism between stationary stochastic approach and Hilbert space generated by single simple path was singled out.

There is rigorous link between probability and the stochastic process framework in the stationary case was established. The case of time variant fraction of time statistics and in order of higher order statistics. At the end the wold isomorphism was extended in the case of cyclostationarityy time series.

A further development of fraction of time probability theory for non-stationary signals were also presented. In paper a more general class of time series were introduced and characterised was name as generalised almost cyclostationarity. The appear has been organised.

Normal concepts and definition of fraction of time framework are reviewed. It is devoted for the construction of confidence bound using the fraction of time probability. The problem with prediction for independence and distributed predicts are now available. There is also simulation experiment that need to be corroborate with the proposed predictors.

The main goal is to introduce concept of confidence bound by using the fraction of probability approach. This approach also helps and allows to use information coming from only one realization of phenomena that comes under the study at the time increasing. The making of the empirical and large sample confidence interval is available and have own implication for the quantile prediction.

The fraction of time approach has many benefits over the classical, stochastic methods. At the very first of all no assumption of observation or stationarity of distribution is needed.

Read More : Fraction Of Time Probability That Exhibit Cyclostationarity